Jan Samarth Mudra Loan Login 2026: The Ultimate Digital Guide to Tracking & Approval

In the rapidly evolving digital landscape of 2026, the Jan Samarth Portal has become the definitive “Super App” for government credit. For millions of Indians, the Jan Samarth Mudra Loan Login is no longer just a web page—it’s the gateway to business scaling and financial freedom.

Gone are the days of manual follow-ups at bank branches. With the integration of AI-driven analytics and real-time data from CBDT and UIDAI, the portal now offers a seamless way to check your Mudra Loan Status and secure approvals in record time.

What is the Jan Samarth Portal?

The Jan Samarth Portal is a unique digital platform that connects 15+ credit-linked government schemes (including PMMY) with over 200 lenders. Unlike traditional methods, this portal uses a single-window interface to verify your eligibility across multiple schemes simultaneously.

Why the 2026 Login is Different

- Unified KYC: Direct integration with your Digital Locker.

- Instant In-Principle Approval: AI evaluates your data to give you a “Yes” or “No” in minutes.

- Direct Stakeholder Connect: Your application is visible to the bank, the Nodal Agency, and you at the same time.

Step-by-Step: Jan Samarth Mudra Loan Login Process

Follow this verified 2026 process to access your dashboard and manage your application.

Step 1: Accessing the Official Portal

Visit the official website: www.jansamarth.in.

Security Tip: Always ensure you see the “https” and the government emblem to avoid phishing sites.

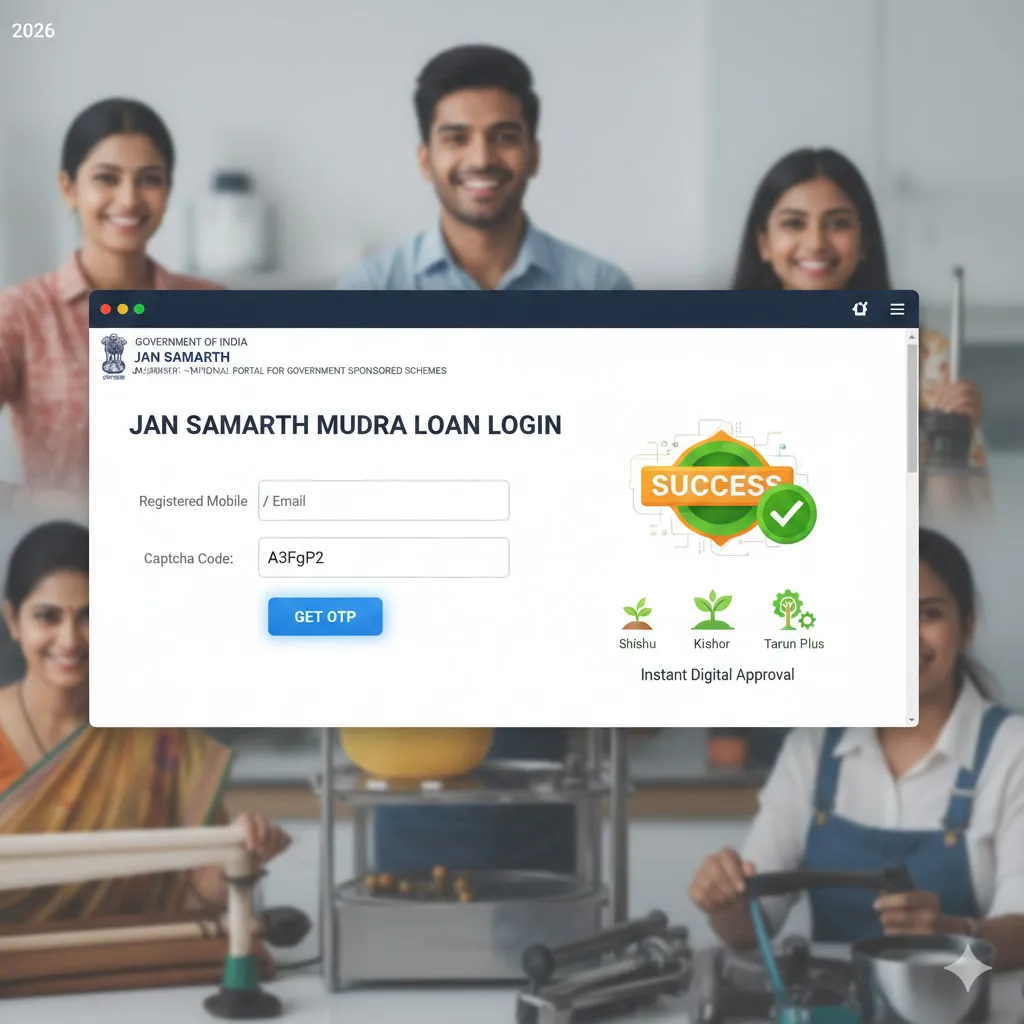

Step 2: The Login Interface

Click on the ‘Login’ button at the top right corner. You will be prompted to enter:

- Registered Mobile Number or Email ID.

- Captcha Code (for bot protection).

Step 3: OTP Verification

In 2026, passwordless login is the standard. You will receive a 6-digit OTP on your registered mobile. Enter the OTP to gain access to your personalized dashboard.

Step 4: Accessing ‘My Applications’

Once logged in, click on the ‘My Applications’ tab. This is where you can view the real-time Mudra Loan Status for Shishu, Kishor, Tarun, or the new Tarun Plus (up to ₹20 Lakh) categories.

Shortcuts to Faster Mudra Loan Approval

If you find the process moving slowly, use these 2026 Shortcuts to speed things up:

- The “Udyam” Shortcut: Link your Udyam Registration Number during the application. The Jan Samarth AI prioritizes Udyam-verified businesses, often reducing verification time by 40%.

- Digital Bank Statement Upload: Instead of uploading PDFs, use the Account Aggregator (AA) framework. This allows the portal to fetch your bank data directly, leading to instant digital approval.

- Pre-Eligibility Check: Before logging in, use the “Check Eligibility” tool on the homepage. This ensures you don’t apply for the wrong category (e.g., applying for Tarun when your turnover only supports Shishu).

Real-Time Tracking: Understanding Your Mudra Loan Status

When you perform your Jan Samarth Mudra Loan Login, you will see one of these status labels. Here is what they actually mean in 2026:

| Status Label | Internal Reality | Recommended Action |

| Digitally Approved | AI has cleared you; the bank is now reviewing. | Download the “In-Principle Sanction Letter” immediately. |

| Pending with Bank | The file is at the branch manager’s desk. | Use the Grievance Shortcut if pending > 7 days. |

| Document Resubmission | KYC or Business proof was blurry or expired. | Re-upload via the mobile app for faster processing. |

| Disbursed | The funds have been released to your account. | Start your repayment schedule to build your credit score! |

Common Login Issues & 2026 Solutions

- OTP Not Received: This is common during peak hours (10 AM – 12 PM). Shortcut: Use the Email Login option or try after 6 PM when server traffic is lower.

- Session Expired: The portal has a strict 5-minute inactivity timer for security. Keep your documents (PAN, Aadhaar) ready before you log in.

- Application ID Not Found: This happens if you applied offline at a branch. Solution: Ask your bank manager to “Digitize the Lead” so it appears on your Jan Samarth dashboard.

Managing Your Loan After Login

The Jan Samarth dashboard is not just for applying; it’s for life-cycle management. You can:

- Download Sanction Letters: Essential for tax purposes.

- Change Preferred Lender: If one bank is taking too long, the 2026 update allows you to “re-route” your application to another interested lender.

- Submit Grievances: If a bank demands collateral (which is illegal for Mudra), use the ‘Grievance’ tab inside your login to report them directly to the Ministry of Finance.

Conclusion: Empowering Your Business Journey

The Jan Samarth Mudra Loan Login is the most powerful tool in an Indian entrepreneur’s arsenal. By leveraging the digital shortcuts of 2026—like the Account Aggregator and Udyam integration—you can turn a weeks-long wait into a 24-hour approval.

Stay proactive, track your Mudra Loan Status regularly, and use the transparency of the Jan Samarth portal to hold lending institutions accountable.